Since I returned from the United Nations in 2012 and became involved in the work of Transparency Institute Guyana Inc. (TIGI) and as a columnist with the Stabroek News, I have been under constant personal attack for the stance I took on governance, transparency and public accountability matters. These attacks and personal vilifications were mainly from the State-owned media as well as from paid letter writers and bloggers, especially during the period 2012 to 2015. For example, on 5 December 2012, Progressive Youth Organisation (PYO), the youth arm of the People’s Progressive Party (PPP), issued a press release condemning the methodology used in arriving at the Corruption Perceptions Index (CPI) for 2012 and in the process singled out me:

Since I returned from the United Nations in 2012 and became involved in the work of Transparency Institute Guyana Inc. (TIGI) and as a columnist with the Stabroek News, I have been under constant personal attack for the stance I took on governance, transparency and public accountability matters. These attacks and personal vilifications were mainly from the State-owned media as well as from paid letter writers and bloggers, especially during the period 2012 to 2015. For example, on 5 December 2012, Progressive Youth Organisation (PYO), the youth arm of the People’s Progressive Party (PPP), issued a press release condemning the methodology used in arriving at the Corruption Perceptions Index (CPI) for 2012 and in the process singled out me:

TIGI’s Vice President is former Auditor General Anand Goolsarran who prior to 1992 was widely suspected to have colluded with the PNC to suppress the production of audited accounts and was complicit in the concealment of PNC mismanagement of Government finances. Mr. Goolsarran has never been held to account for his failure to conclude audits prior to 1992. In addition, his personal association with AFC leader Khemraj Ramjattan is widely known, he has made frequent appearances at the AFC public events.

Setting aside for the time being the false accusations made about me, the above statement demonstrates a fundamental lack of understanding on how the CPI is computed and who is responsible for compiling it. As stated in several of our columns, the Index is calculated based on surveys carried out of the perceptions of knowledgeable people, such as senior businessmen and political country analysts, of perceived levels of corruption in a country. The results, when computed using statistical methods, correlate well and provide some confidence about the actual levels of corruption. The responsibility for compiling the CPI is that of Transparency International, headquartered in Germany, and its local affiliate TIGI plays no part in the process.

At a Commonwealth Parliamentary Association seminar held around 2016 or 2017 at the Marriott Hotel, the then Speaker of the National Assembly invited me to make a presentation. The current Attorney General was there, and in his opening remarks, he referred to my presence, repeated the false accusation made by the PYO, and boasted that the country’s accounts are now audited every year. Little did he realise whose efforts it was that saw a restoration of public accountability after a ten-year gap. During the break period, the Attorney General and I sat close to each other, and I took the opportunity of clarifying to him that the date of my appointment as Auditor General was 31 December 1990. Ms. Indra Chandarpal, a long-standing PPP Member of Parliament, sat next to us, and I asked her to confirm the date, which she did. The Attorney General shrugged his shoulders as if nothing happened!

The latest salvo came a few days ago from none other that the Vice President and PPP General Secretary, Mr. Bharrat Jagdeo at a press conference at Freedom House and at a PPP rally in Port Mourant on the Corentyne. He stated, again quite falsely, that I was Auditor General for most of the ten years prior to 1992 during which period not a single set of audited accounts was produced for the country. He then suggested that I should have resigned if I had integrity; the job of the Auditor General is to audit the public accounts of the country; and if I did not produce audited accounts, then I did not have a work job. He then added that from 1992 to 2023, every single year there were audited accounts and that prior to 1992, the last set of audited accounts was in respect of 1982. In fact, the last set of audited accounts prior to 1992 was in respect of 1981 and not 1982. Similarly, in the post-1992 period the last set of audited public accounts was in respect of 2021 and not 2023. The Vice President went on to further state that I sat on the job for eight of the ten years when there were no audited public accounts. That puts my appointment as Auditor General around 1984 when in fact I was Senior Internal Auditor at the Guyana State Corporation at the time!

The Vice President appears to display a lack of understanding about the role of an external auditor of an organization. Unless the entity produces financial statements for audit there can be no audited accounts. Is this the fault of the auditor and should the auditor resign? In the private sector, auditors are appointed annually at annual general meetings of shareholders, and it would be entirely appropriate for the auditor to resign if he/she is unable to perform the duties he/she is contracted to do. The situation is, however, quite different as regards the appointment of the Auditor General who is the holder of a constitutional office. Once appointed, he/she serves until retirement on attaining the age of 65. The Auditor General cannot be removed from office except for inability to perform or misconduct in office. If I was not performing as Auditor General, why is it that the late President Jagan or the Vice President when he served as President, did not take steps to remove me from office?

That apart, it is the responsibility of the Minister of Finance to prepare and submit to the Auditor General draft financial statements constituting the public accounts not later than 30 April each year. The Auditor General then audits these statements and submit his report to the Assembly by 30 September. In the pre-1990 period, the last set of draft accounts to be submitted to the Auditor General was in respect of 1981. These were duly audited, and the related report was laid in the Assembly in December 1987, at a time when I was not the Auditor General.

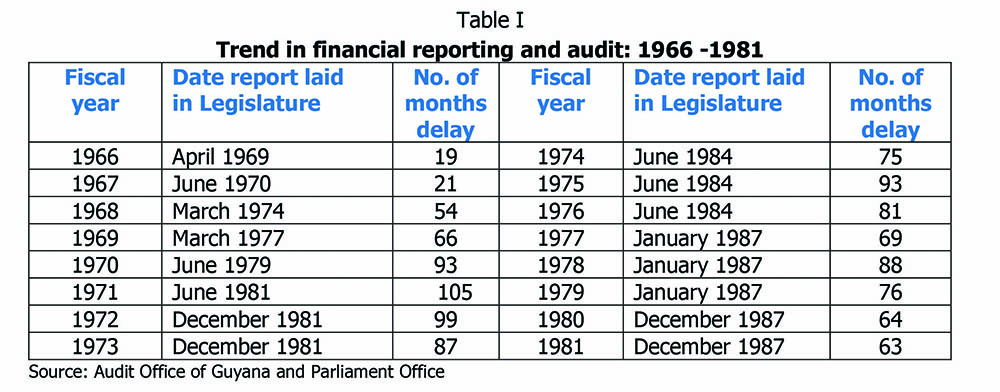

Financial reporting and audit: 1966-1981

Experience has shown that undue delays in having audited accounts of an organization are an indicator that all is not well with its financial management systems and procedures and are symptomatic of a more fundamental problem. In relation to the public accounts, the average delay was six months during the pre-Independence period 1953 to 1965. However, for the years 1966 to 1981, such delays were in the order of on average six years, as shown at Table I:

As can be noted, the greatest delay was in respect of the year 1971 when the accounts were not finalized and presented to the National Assembly until June 1981, almost nine years later. To compound matters, a number of years were reported together: 1972 to 1973; 1974 to 1976; 1977 to 1979 and 1980 to 1981. It soon became clear that the inevitable was likely to happen. Public accountability was eventually brought to a standstill at the end of 1981. The Authorities had contended that the main frame IBM System 3/15 mainframe computer at the Ministry of Finance had “crashed”, resulting in the Government’s inability to produce the public accounts for subsequent years.

The Hoyte Administration had inherited seven years of the backlogged accounts covering the period 1977 to 1983. To its credit, it was able to produce audited public accounts for first five of these years in 1987, albeit in combined form.

Restoration of public accountability

Contrary to the impression given by the PYO, the Attorney General and the Vice President, I was appointed Auditor General on 31 December 1990. I immediately drew the attention of the Minister of Finance, the Accountant General and the concerned senior officials about the requirements of the law relating to financial reporting of the Government and the fact that the said law was honoured in breach for eight years. The Accountant General was adamant that computer problems prevented him from finalizing the public accounts for not only the backlogged years 1982 to 1989 but also the year in question – 1990. On the other hand, Accounting Officers contended that it was the responsibility of the Ministry of Finance to process transactions relating to their Ministries and Departments and to submit periodic printouts for reconciliation with their records. Because of the absence of such printouts, these officials contended that they could not carry out the necessary reconciliations and therefore could not prepare their appropriation accounts and submit them for audit. It soon became clear that political intervention was needed to redress the situation and to break the impasse.

The Audit Office had conducted preliminary audits of Ministries and Departments and had held its findings in abeyance, pending the submission of financial statements. I took the view that in the absence of financial statements, the results of the preliminary audits should be presented to the Legislature. The Government vigorously opposed this view, prompting me to seek a legal opinion from the Attorney General on the matter, which opinion supported my view. As a result, the Audit Office issued preliminary reports to the National Assembly for the years 1982-1985.

In late 1991, I wrote to the Minister outlining the problems associated with the Government’s financial management and made several recommendations, including a proposal for a two-pronged approach to restart financial reporting, with 1991 as the cut-off year. The key recommendations were:

(a) The closure of all government bank accounts and the opening of new ones with effect from 1992 to avoid any contamination with the backlogged years;

(b) Instituting proper systems and procedures to ensure accurate recordkeeping and reconciliation, and to facilitate timely, reliable, and accurate financial reporting for the future, commencing 1992; and

(c) The setting up of a task force to deal with the backlogged accounts covering the period 1982 to 1991.

The Accountant General had estimated it would take approximately six months for each of the backlogged years to be finalized. In other words, it would have taken until 1997 to bring the backlogged accounts up to date, by which time the current year’s accounts would have gone backlogged by five years, hence the recommendation of a two-pronged approach. Although the Minister accepted the above recommendations, they were not implemented despite strenuous efforts by the Audit Office to influence the Ministry of Finance to do so.

In late 1992, I renewed my representations with the new Minister, and met with the then Head of the Presidential Secretariat (HPS) and the Accountant General to present my arguments in favor of a resumption of annual financial reporting based on the two-pronged approach I had advocated. The Accountant General contended that it was unprecedented to have a gap in financial reporting and that any attempt to do so would result in inaccurate reporting. The HPS enquired about the level of accuracy that could be achieved if my recommendations were to be followed. The Accountant General indicated that such accuracy would be in the vicinity of 60-70 percent to which the HPS responded: Would a 60-70 percent level of accuracy not be better than no financial reporting? The Accountant General became silent!

In February 1993, the Government issued instructions to the Accountant General and Accounting Officers to comply with the requirements of the law relating to annual financial reporting of the public accounts. As a result, financial statements for the fiscal year 1992 were submitted for audit examination. However, such submissions were not without their fair share of resistance and lack of cooperation from those responsible for preparing the accounts. As was expected, the accounts were somewhat incomplete in that, of the 12 consolidated statements comprising the public accounts, two were not submitted. However, individual statements of revenues and expenditures of all Ministries and Departments, which numbered approximately 200, were submitted. The Audit Office completed the audit of these statements and accounts, and I presented my report to the Minister on 14 September 1993 for laying in the Assembly, thereby bringing to an end ten years’ absence in financial reporting at the national level. It was a hard-fought victory for the restoration of public accountability. Since then, there have been annual financial reporting and audit, and laying of the related reports in the Assembly.

In relation to the backlogged accounts for the years 1982-1991, a task force was set up to compile the financial statements. However, little progress was made, and the effort had to be abandoned, resulting in a significant blemish in the history of public accountability in Guyana.